Start Your “Real Estate Empire” Today

Without buying a single piece of property ...

In this issue of Investing Daily Dose (IDD):

🏠Rental Income Without the Hassle🏠

True Wealth Builders do lots of things right.

They invest in companies with powerful storylines.

They invest for the long haul.

They look at “income” as “cash flow.”

And they look at the numbers, which say owning a home instead of renting is the way to go.

The proof: A typical homeowner’s net worth is 40 times higher than that of renter, according to a 2023 study by the National Association of Realtors (NAR).

Call it the “Real Estate Wealth Effect.”

And there’s a logical “new angle” some folks try after they see the value of their home climb: Buying a house and becoming a landlord.

The hoped-for financial benefits of renting out a home are simple:

You generate steady income.

And the renter pays your mortgage, building your equity (which also gets magnified by the property’s growing market value).

On your list of “pros and cons,” those are definitely the “pros” – and powerful they certainly are.

It’s when you start penning your “cons of being a landlord” list that you discover how many negatives there can be.

If you don’t want to deal with tenants directly, you’ll have to hire a property manager – taking a hefty bite from that monthly rental stream you get.

You can save some money by managing the property yourself, but those savings plummet and migraines increase if you end up with a “tenant from hell” who pays late, doesn’t pay at all – or gets evicted and engages in “revenge damage” before you get them off your property. (If that happens, you can also add a splash of “legal fees” to your property expenses.)

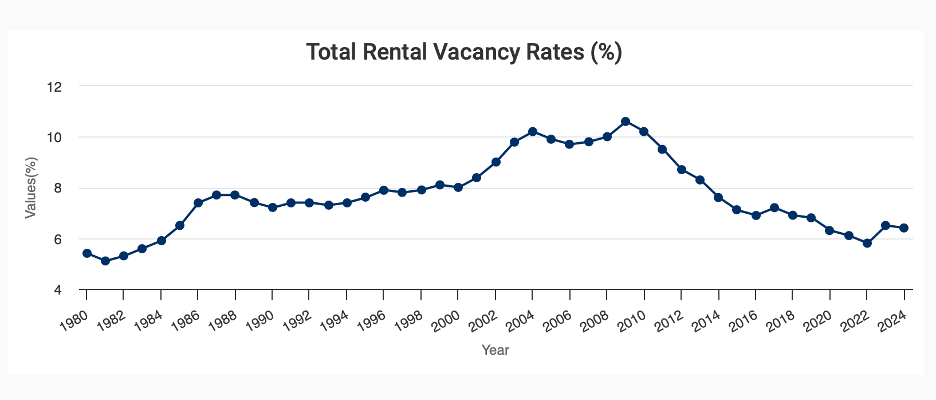

And what if you can’t find tenants … or, at least, can’t find them immediately? Then you have to cover that mortgage yourself – for however long it takes. Rental vacancies are about 40% lower than in the Great Recession era peak of 10.6% (2009).

But they are edging up – from 5.8% in 2022 to 6.4% in 2024.

And, by the way, don’t forget about that 20% down payment.

As of December 2023, the average down payment for a U.S. home was $51,250. And they’ll keep getting higher: NAR Chief Economist Lawrence Yun just said he expects U.S. home prices to rise between 15% and 25% over the next five years.

The rewards for joining “The Landlord Club” can be very high. But that down-payment entry fee can actually serve as a barrier to entry, the dues can be expensive if you don’t have that dream tenant, and the membership costs can be pricey if there are big expenses to cover.

Fortunately, there’s another way to be a Wealth Builder in real estate – without owning a single property.

Bill’s Investing Takeaway

“This topic fascinates me … because of my family experiences in real estate ... but also because my work here gives me a great place to observe investor behavior. And that behavior can be intriguing since there’s a ‘right way’ to do things … and a ‘wrong way.’

Like with ‘passive income.’

True passive income is like ‘cash flow.’ And that ‘passive’ prefix should mean you don’t have to do lots to get it.

I mean … let’s say you decide to become a landlord. People do it all the time – a family member is a landlord, and has been for 20 years, and has done exceptionally well. But I also see folks who got into rental housing as a means of having passive income – and I see them get keelhauled by a bad real estate investment.

Still, real estate can be a wonderful investment – as mentioned earlier, NAR Chief Economist Lawrence Yun sees a continuation of the healthy price appreciation that’s been the norm for many years … he’s talking about a potential 15% to 25% increase in U.S. home prices over the next five years.

Given the underlying strength in the U.S. housing market, I can also see that.

So how can you hitch a ride on that price gain … and draw off some true passive income – let’s say, 14% a year on your money … year in and year out?

The only effort you’ll have to expend is the energy you put into looking up the ticker symbol I’m happy to tell you all about here.”